If you’ve been putting off creating an estate plan because it seems too time consuming, here’s a basic step-by-step guide to help streamline the process.

Step 1: Establish Your Goals & Objectives

Since everyone is different, the goals and objectives of your estate plan need to be clear. Some people may simply want to ensure their assets are distributed according to their wishes. Others may be more concerned about minimizing inheritance taxes and passing on a legacy. No matter what your objective may be, it serves as the foundation of your plan.

Step 2: Create Your Last Will & Testament

When you have a Will, you decide how your assets will be divided. If you have young children, it lets you choose their guardian – not the family court. You can appoint someone to be your executor and carry out your wishes. Otherwise, probate court will decide.

Step 3: Establish A Living Trust

Though there are many types of legal trusts, a valid Living Trust helps your family avoid probate court and can facilitate a faster distribution of your assets to your heirs. It can also be used to manage your estate before you die because the trust owns your assets and you can name yourself as trustee.

“Non-federal assets that require a beneficiary are 401(k)s, IRAs, private sector insurance policies, and banking accounts.”

Step 4: Update Your Beneficiaries

A beneficiary designation supersedes a Will, Trust, or pre-nuptial agreement and bypasses the probate process. This is why it’s important to update all beneficiary forms. As a federal employee, your designated beneficiary is paid a death benefit for lump sum FERS payments, unpaid compensation, your Thrift Savings Plan (TSP), and the Federal Employee’s Group Life Insurance (FEGLI). Non-federal assets that require a beneficiary are 401(k)s, IRAs, private sector insurance policies, and banking accounts.

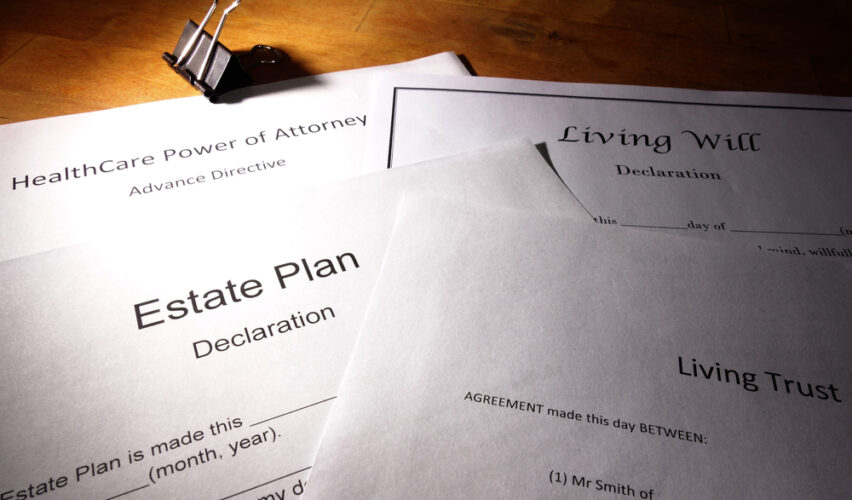

Step 5: Create A Durable Power of Attorney (DPOA)

Another key element of an estate plan, a Durable Power of Attorney remains in effect if you become incapacitated or unable to make decisions for yourself. With a comprehensive DPOA, you can select an agent and direct them to make specific decisions about your property, finances, investments, and bills, and they can sign documents on your behalf.

Step 6: Create Advance HealthCare Directives

When a medical crisis leaves you incapacitated and unable to make decisions for yourself, advance healthcare directives help ensure your preferences are respected. It’s important to check which documents your state law requires. For example, a Living Will describes your preferences for healthcare treatment while a Durable Power of Attorney for HealthCare names the person you’ve chosen to make healthcare decisions for you.

To learn more, reach out to an FRC® trained advisor.